September 2018

Medikit is a major manufacturer in vascular access and interventional medical devices. In many ways, the company embodies characteristics that we look for in an investment: market-leading position in a small niche, a steady stream of recurring sales, and strong balance sheet. As in the case with EM Systems, Medikit has practically no sell-side coverage and files exclusively in Japanese. As such, this gem of a business has flown under the radar of larger institutional investors.

A Japanese “Mittlestand”

Medikit was founded in 1973 by Mr. Hiroaki Nakajima who personally owns ca 19% of the company today. Combined with his holding company Nakajima Corporation, the Nakajima family continues to hold 55-56% of shares today, which is highly impressive.

The company has over 50% market share in Japan for its two core products:

- Catheters for kidney-dialysis treatment, which account for approximately a third of total sales

- Intravenous (IV) catheters with a special valve that prevents the reverse flow of blood upon insertion

We at Lacuna place a premium on holding companies such as Medikit because of their strong business model. First off, the dialysis catheter industry itself is an excellent business, as there are over 300,000 kidney-disease patients in Japan who need on average four dialysis treatments per week and two catheters each time. Secondly, the needles are considered “Critical components”: as a percentage of a dialysis system’s cost, the price of a needle is de minimis; however, the needle’s role absolutely crucial.

These traits allow for a steady recurring stream of revenue from a large (and increasing) total addressable market (“TAM”), as well as a fat and remarkably stable margin over decades of operations.

As such, Medikit fits a classic “mittlestand” profile: while Medikit might only have a market capitalization of €400 million, its founder-led and market-leading position in niche applications of catheters makes it a hidden champion that we are comfortable holding.

“Boring is Beautiful”

When it comes to investing, many investors look for spectacular growth targets and flashy investor presentations. However more often than not – as we learn from Warren Buffett – boring can in fact be very beautiful. In the case of our investment in Medikit, that has certainly proven to be the case: as of August 28, 2018, we are currently up +22% on our position since buying in at the start of our fund’s management overtake in December 2017.

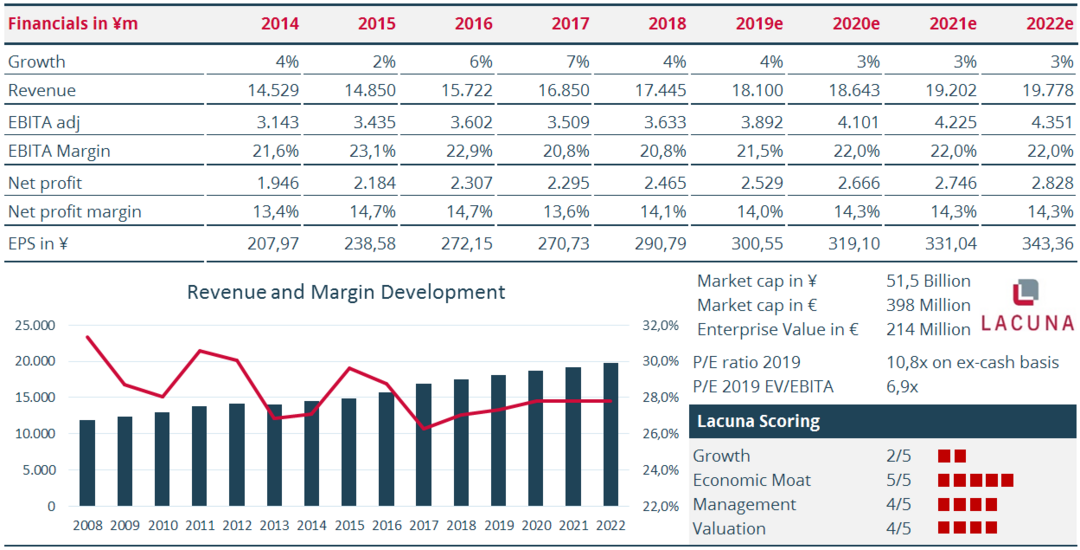

The overall thesis of the business is very straightforward. In addition to being a high-quality business as aforementioned, we were also able to take advantage of the company’s under-the-radar profile and purchase Medikit at a very good valuation. While the top-line growth in the business is only around +3% per annum, the multiple expansion story is much more interesting: the company only trades at 7x forward adj. EBITA, an absolute bargain for the quality of this business.

We are further also comforted by Medikit’s fortress of a balance sheet: currently, cash makes up 50% of the total company’s market capitalization. While Western investors are typically not partial to such a large cash pile, it is important to keep in mind that the Asian – and especially Japanese – mindset is to be very conservative with the company’s use of cash.

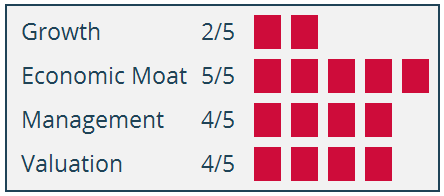

That is absolutely not to say that we at Lacuna are fond of “cash hoarding” as a capital allocation strategy. We believe that Medikit’s management are certainly conservative, but do not fall in this category. In addition to the fact that the founder-led team is already very much incentivized to perform, Medikit has increased dividends twice in the last couple of years and has also bought back 10% of its stock when it was trading at 2x EV/EBIT.

Summary

These activities are very rare among Japanese companies, and give us confidence that management are mindful of its shareholders. Based on this track record, we actually find that Medikit’s management in fact has a quite decent track record in capital allocation, and continue to be aligned alongside the team.