July 2018

Strides Shasun (“Strides”) is an Indian mid-cap generics manufacturer with a focus on United States and Australia. While the business sells the lion’s share of formulations in regulated markets (71%), almost a third of sales falls into institutional sales (20%), which include drugs for HIV, Malaria and Hepatitis C, and Emerging markets (9%).

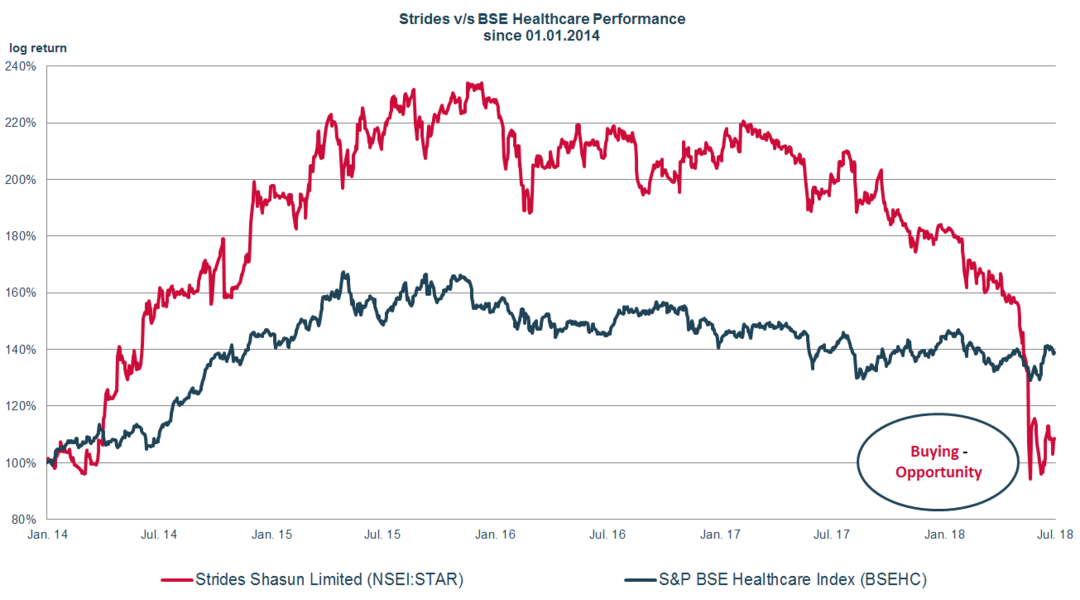

Strides’ share price has corrected by 50% since the beginning of 2018 driven by an earnings miss caused by delayed product approvals and a general negative sentiment surrounding generic drugs business models. Our view is that these are short term cyclical issues which have limited impact on the long term value of the company, letting us take advantage of the market’s irrational behavior. We feel comfortable betting on this dark horse which has compounded returns at a 20%+ CAGR for shareholders over the last decade.

Management Without a Golden Parachute

Arun Kumar, current CEO, is accredited as a deal maker and a good capital allocator. Arun is a first generation entrepreneur who, after working for a pharmaceutical company for 8 years, setup Strides in 1990. Arun has a keen eye for buying businesses below intrinsic value and selling when he gets a great price. For example, in 2013 he sold the Strides injectables unit to Mylan for $ 1.6 bn at 20x EV/EBITDA and distributed cash among shareholders, making it the third largest pharmaceutical deal in India at that time.

Arun believes in building business through a differentiated strategy. When the Indian generic pharma companies were chasing growth in the US during 2010-2016, Arun realized that the market was overcrowded. Therefore, he decided to foray into Australia to tap the growing generics market and capitalize on the government’s push to generics. This strategy has played out well as the division recorded double digit growth. Recently, Strides has been discussing to acquire the number 1 player in the Australian generic market to establish a dominant position in the region.

Arun owns a third of the business, thus giving us the confidence that he has enough skin in the game to execute a successful turnaround.

A Perfect Storm

Strides’ current quarter was nothing short of a perfect storm. Strides missed its latest quarter’s earnings due to a mix of internal and external factors. The Company fell short of its targeted US revenues, which makes up 27% of revenues, due to

- a delay in product approvals by the US FDA, and

- an increase in competition in its existing product portfolio.

However, our research finds that management has been working quickly to acquire the approvals from the FDA and over the last few months has successfully gotten approvals for four new products. Furthermore, management has decided to reinforce their US branch by setting up a direct marketing presence instead of third party marketing.

As for the institutional business, which accounts for 20% of total revenue, Strides faced a setback due to funding cuts from donors. Our opinion is that this is an industry wide issue which affects all players. It will take the company a few years to build growth in this business.

On the positive side, Strides had some successes in Australia, which make up 32% of revenues. There, revenues grew by 15% and margins expanded by an astounding 300 bps, largely due to operating leverage from the Indian facilities. With its latest acquisition, the company intends to accelerate the pace of this consolidation.

Strides has a leveraged balance sheet at (4x Net Debt/2019 EBITDA) which may initially seem alarming, but our view is that the leverage ratio appears high as the 2019 EBITDA was impacted by one-time issues in the US. We believe that these business challenges are temporary as the EBITDA is expected to grow by 30% by 2020 and not significantly impair our long term intrinsic value of the business.

Our Variant View

We continue to believe in the business for the following reasons:

- The markets continue to have a negative perception of the US generic pharma business which we believe is overdone as the last three years of supply side consolidation have squashed margins of generic manufacturers across the board. We estimate to likely be near the bottom of the business cycle where we think rationality will prevail and generic companies will exit losing deals and enter price negotiations with suppliers. For example, managements of larger generic companies, such as Teva and Sandoz, have been quite vocal about exiting low margin products during their latest management calls.

- Strides faced the market’s ire as markets assigned undue weight to short term results. We assume the business issues faced by the company to be temporary and without a major structural impact. Furthermore, we expect 2020 to be a revival year for the company by when the impact of management turnaround efforts should be clearly visible, such as increased product approvals and leadership consolidation in Australia.

- Lastly, we think the current CEO is the best person to lead the turnaround of the company. Strides did not have other issues such as FDA sanctions which impacted many of its peers. Under his leadership the company delivered index beating returns for the last decade.

Summary

While Strides faces an ongoing decline in performance, we expect earnings to improve soon. The key catalyst that would drive earnings would be FDA approval for pipeline products, leveraging a dominant position in Australia to extract margin improvement and turnaround in the US business.